I’m Unwilling To Change The Rules Of FIRE To Win The Game

16 min readI’ve been documenting my journey in Financial Independence Retire Early (FIRE) since July 2009. I’m not aware of any other blogger who commenced their FIRE journey earlier, is still currently retired or unemployed, and has maintained a consistent writing presence like I have on Financial Samurai.

When I began sharing my FIRE experiences, I was a 32-year-old investment banker in equities, grappling with burnout after 11 years in the field. As time passed, the allure of the business dwindled.

The global financial crisis left a lasting impact, with numerous friends and colleagues losing their jobs, and clients understandably becoming more demanding and anxious. Concurrently, chronic pain in my back, legs, and jaw frequently reached debilitating levels.

In light of these challenges, I wanted out.

This post will discuss:

- The three rules of FIRE

- Why we like to change the rules of FIRE

- My financial journey and the challenges I faced

- Why I’m unwilling to include active income to win at FIRE

- The importance of enjoying your financial independence journey

- Why you should embrace the first rule of FIRE, even though there is temptation not to

The Most Important Rule Of FIRE

To truly achieve financial independence, I established a crucial rule for attaining FIRE:

To be deemed financially independent, one must amass sufficient investments capable of generating passive income that covers basic living expenses.

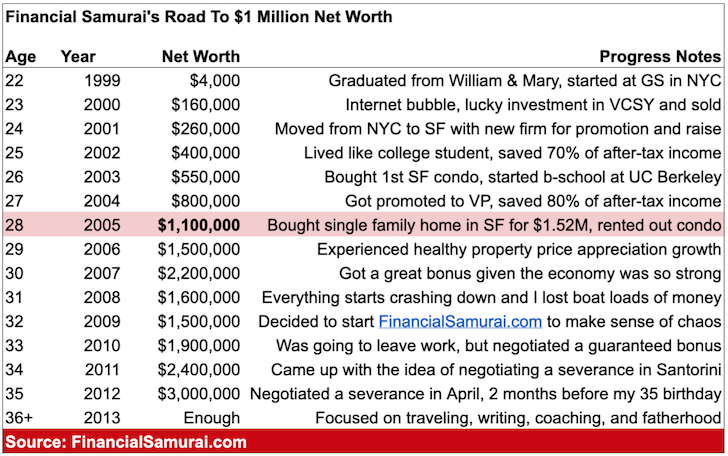

I instituted this FIRE rule in 2009 for myself and anybody else who wanted to follow. Then dedicated two years and nine months to achieving it before retiring in March 2012. The last of my WARN Act pay finished in June 2012.

Upon retirement, my net worth stood at approximately $3 million. Excluding the equity in my primary residence, my investable net worth was closer to $2.4 million.

This $2.4 million generated around $80,000 per year in passive income. With no dependents and a fixed-rate mortgage, I could cover my basic living expenses in San Francisco. Although, as you’ll read on, I wasn’t truly comfortable during my initial years of FIRE.

The Second Rule Of FIRE: Negotiate A Severance

Thousands of Financial Samurai readers, and many more, embraced my primary rule of FIRE. The movement gained momentum when other bloggers, such as MMM, joined and contributed guest posts on Financial Samurai three years later to help spread the word.

The second rule of FIRE that I advocated is to always attempt to negotiate a severance package. The rationale behind this is that if you are planning to quit your job and retire early, it’s worthwhile to try negotiating a severance package as a parting financial gift. There is no downside.

Upon my retirement in March 2012, I successfully negotiated a severance package that equalled five years’ worth of regular living expenses. This negotiation proved to be one of the most rewarding and unexpectedly satisfying revelations of my employment history because I wasn’t initially sure it was possible.

Drawing from this experience, I authored the bestselling ebook, “How To Engineer Your Layoff,” aiming to assist others in following the second rule of FIRE. Receiving a severance package from a job you wanted to quit anyway feels like winning the lottery.

Over the subsequent twelve years, thousands of readers of the book shared their severance negotiation experiences. Consequently, I continually update my book with new strategies and situations to empower more individuals to break free from a job with money in their pockets. HTEYL is now in its 6th edition.

People Are More Fearful Of The Second Rule Of FIRE Than The First

Due to a combination of misconceptions and a fear of confrontation, my second rule of FIRE did not gain as much traction as my first rule. Ironically, I believe it’s actually easier to have a heart-to-heart conversation with your manager to negotiate a severance than it is to generate enough passive income to cover your basic living expenses.

However, I understand why people might be apprehensive about trying to negotiate a severance package. In our current technological age, where social interactions often occur more on our phones and laptops than in person, breaking up over text and ghosting have become more common.

While technology has its benefits, it has also diminished our in-person social skills and courage. When these skills are underutilized, negotiating a severance can seem intimidating, even with a detailed guide to help you through the process.

For those who identify as keyboard warrior introverts, a common trait among personal finance bloggers, there may be more resistance to attempting a severance negotiation.

Many bloggers and podcasters in the FIRE movement chose to quit their jobs rather than negotiate a severance. It’s easier to do so. Consequently, suggesting that people logically try to negotiate a severance may serve as a reminder of their own reluctance to do so.

Wanting To Change The Rules Of FIRE Is Understandable Because Achieving FI Is Hard

I get it. Achieving financial independence my way is hard. But good things aren’t supposed to come easy. If you get something easily, you will take it for granted. Let’s not change the rules just because we lack patience or determination.

Since securing my first job at Goldman Sachs in August 1999, I’ve been diligently saving with the goal of early retirement. After just a month of consistently working from 5 am to well past 7:30 pm, I realized I couldn’t sustain this pace until my 60s. Consequently, I adjusted my goal to retire by the age of 40 in 2017.

While I didn’t quite make it to age 40, my early retirement was facilitated by a severance package. Recognizing that the severance would cover over five years of living expenses, retiring at 34 with a severance felt akin to retiring without one at age 39. The timing was close enough.

Despite having a financial safety net in the form of a severance, I still harbored nervousness about retiring at such a young age. It seemed unconventional to relinquish a six-figure job in my mid-30s, a time when careers typically gain momentum. Nevertheless, I identified my “enough” amount and chose to take the leap of faith anyway.

This is when I became tempted to change the the definition of FIRE. My fear and uncertainty over whether I made the right move took over.

The Start Of FIRE Subtypes: Barista FIRE, Lean FIRE, Wife FIRE

My safety net was my wife, who is three years younger than me. I conveyed to her that if FIRE worked out for me after three years, she too could retire by age 35. In the interim, it made sense for her to continue saving and investing while taking advantage of subsidized healthcare benefits, especially as we were contemplating starting a family.

Around 2012, the year I left my job, marked the emergence of Barista FIRE, Lean FIRE, and Wife FIRE.

Barista FIRE is a type of FIRE where individuals work part-time or lower-paying jobs to bridge the gap between their passive income and expenses. A common example is working as a barista at Starbucks, where employees often receive subsidized healthcare insurance, a significant hurdle for those aiming to retire early.

Lean FIRE is a FIRE approach involving living on a bare-bones budget to facilitate early retirement. An extreme example is Jacob from ERE, who lived on a boat and spent only $7,000 a year for a couple of years before transitioning to become a quant trader in finance. Others, typically without children, might opt for the van life, traveling around the country.

Then there is Wife FIRE, a financial independence strategy where men rely on their wives to work, allowing them to retire early. It’s a fascinating shift as more women become breadwinners. Some men find it uncomfortable to say they are a stay-at-home dad.

Bending The Rules: Three Years Of Hybrid FIRE

Even though I could have sustained myself with $80,000 a year in passive income, I likely wouldn’t have pursued negotiating a severance at age 34 if my wife had not continued to work. In that scenario, I likely would have persevered working until 2017, the year I turned 40. I wanted another $500,000 – $1,000,000 in investable assets.

During the period from 2012 to 2015, I found myself living a hybrid lifestyle encompassing elements of Barista FIRE, Lean FIRE, and Wife FIRE. I embraced a frugal lifestyle, even contemplating the sale of our house in 2012. Meanwhile, my wife persistently earned, saved, and invested. Additionally, from 2013 through early 2015, I engaged in part-time consulting work for Personal Capital, now known as Empower.

Was this changing the rules of FIRE? More like bending the rules because I was unable to feel 100% settled on $80,000 a year or passive income. After one year of true retirement of traveling and dilly dallying, I wanted to consult again for excitement and for supplemental income.

The Next FIRE Challenge Begins: Dual No-Income Household

In 2015, at the age of 35, my wife finally joined me in early retirement. We were now a dual no-income household (DNIH).

Initially hesitant to negotiate a severance package, she questioned, “Why would my employer lay me off with a severance package when I’m a good employee?” Despite her reservations, being a woman with over 10 years of service made her one of the best candidates in my studies.

She successfully negotiated a hybrid severance package that ultimately exceeded $100,000 in value. For more details on how we achieved this, you can refer to the post, “How To Negotiate A Severance Package As A High-Performer.”

Presently, my wife remains out of the traditional workforce, engaging in many tasks such as editing my posts and podcasts, handling back-end work for FS, and dedicating time to raising our two young children. It’s a full-time job being a parent. But there will be a void to fill once our daughter goes to school full-time in September 2024.

Both partners not having a day job with healthcare benefits is tough to do. But thanks to three years of hybrid FIRE, we made it happen. However, once we had kids two years later, FIRE got even harder.

I Don’t Want To Change The First Rule Of FIRE To Win The Game

I provide this background on FIRE and our FIRE journey to offer perspective before sharing what comes next.

As one of the original architects of the financial independence movement, I am steadfast in my commitment to maintaining the integrity of the first rule of FIRE, both for my benefit and yours.

In response to comments on my post about blowing up my passive income for a house, some have suggested incorporating active income to regain my financial independence. However, I consider this approach to violate the first rule of FIRE.

If you require active income to cover your living expenses, you are no different from a person who has to work for a living! In this situation, you are not FIRE.

These Posts Don’t Write Themselves

These posts do not materialize effortlessly—they demand hours of dedicated writing and undergo at least 50 revisions before publication. Even after publishing, ongoing updates are required, and there are comments to approve and respond to. Give writing a 3,000-word post a try yourself and you’ll see.

I also don’t regularly write affiliate posts for search engines, a common practice among bloggers seeking online income. Instead, my content revolves around the intersection of money and life, often lacking a direct income component.

I also operate without a paywall or donation option. My primary motivation is the enjoyment derived from building a community, discussing interesting topics, learning from each other, and creating something out of nothing.

Recognizing that there will be a time when I lose the motivation or health to write, I am mindful that relying on active online income to sustain my life and family in such a scenario would be problematic.

Consequently, after accounting for business expenses—of which there are many when running a website—I strive to reinvest 100% of my active income into building sustainable passive income.

Why You Don’t Want To Take A Shortcut On Your Way To Financial Independence

Taking shortcuts can be tempting. But if you take shortcuts, you will only be hurting yourself.

Here are the reasons why true financial independence is achieved only when you have enough passive income to cover your basic living expenses. Resorting to the easier routes, such as incorporating active income, relying on a working spouse, or changing the definition of FIRE, is not the way.

Changing the rules of FIRE may:

- Strip away your sense of pride and satisfaction derived from achieving genuine financial independence after a long journey.

- Result in having less wealth than necessary to attain financial security.

- Halt the challenge of continually creating and producing value for society, for both you and your spouse.

- Jeopardize the safety and security of your children due to potential conflict at home. If you’re trying to trick yourself into FIRE, then you may feel more financial stress given you aren’t really FI.

- Lead to feelings of failure and shame for altering the rules to accommodate your progress. Deep down, nobody feels good beating a game if they didn’t win by playing on the same playing field.

If you alter the rules of a game to secure a victory, you may experience temporary happiness at most. However, this could be followed by a lingering sense of emptiness because the victory wasn’t achieved in the right way.

Feedback From People Who Took The Shortcut Approach To FIRE

I spoke to someone who identifies as Coast FIRE, and they candidly admitted that it served as a way to feel better about not being further along on their financial journey. Recognizing that Coast FIRE is essentially no different than a working person with retirement savings, they acknowledged overspending in their 20s and 30s, putting them behind their peers.

I spoke to a dad whose wife works as an optometrist making six-figures. He tells his buddies he retired early, but deep down, he feels bad he’s not the provider for his family. His wife has worked for over 10 years since he retired early. Despite regularly playing pickleball at his private club, he feels his life lacks purpose and meaning. At least he’s a damn good pickler.

As a Financial Samurai, the philosophy is not to rig the game in your favor, even though others may do so. Instead, the approach is to respect the rules of engagement. Embrace hard mode. It’s not like we’re battling on the beaches of Normandy. The worst thing that happens by following the rules of FIRE is that it just takes longer than desired.

While I arbitrarily established the first rule of FIRE in 2009 when starting Financial Samurai, I do not claim to be the ultimate authority on FIRE. However, after 15 years of writing about FIRE, my first rule has become established and accepted by millions. Let’s embrace the challenge.

The Third Rule Of FIRE: Use A Multiple Of INCOME Not Expenses

Finally, allow me to highlight another way in which my approach differs from the majority when it comes to establishing a target net worth figure. The divergence lies in whether one uses expenses or income as a variable to determine their target FIRE net worth.

Using EXPENSES As a Variable to Establish a Net Worth Target

Most individuals adhere to the 25X annual expenses guideline before claiming financial independence. It is the inverse of the 4% Rule from the mid 1990s, which is outdated.

For instance, if your annual expenses amount to $40,000, achieving a net worth of $1 million is deemed reaching FIRE. However, the reality is that you need $1 million worth of investments, which, when withdrawn at a 4% rate, can cover your $40,000 annual expenses. Factoring in taxes, you actually need closer to 30X annual expenses.

The 25X guideline reveals the intricacies of determining financial independence, but I take it a step further by introducing a multiple of income.

Using INCOME As a Variable to Establish a Net Worth Target:

I advocate for individuals to aim to accumulate at least 10X and ideally 20X their average annual income over the past three years to achieve financial independence. I incorporate income as a variable because it keeps FIRE enthusiasts challenged. The more you earn, particularly as your career progresses, the more you must save and invest to meet your target net worth.

With the income method, it’s more challenging to “cheat” your way to financial independence by drastically reducing your expenses. While cutting expenses to boost saving and investing is foundational to FIRE, claiming financial independence on $500,000 simply because you live with your parents and have reduced expenses to $20,000 may not be a sustainable lifestyle. Your dad will eventually kick you out.

I write for the majority of people who don’t want to retire early and live in poverty. Instead, most readers have hobbies, enjoy socializing, love to travel, and perhaps aspire to start a family one day. Allowing room for growth is why using an income variable is more realistic.

To be clear, both using expenses or income to determine your FIRE number is acceptable, as both approaches can lead to the same FIRE number. However, focusing on income adopts a growth mindset, which is more powerful for building wealth.

The Honor Of Following The Rules Of The Game

During my high school coaching days, I was watching a match when my player called an in ball out. I overruled him because I wanted him to play with honor. The ball he called out was clearly in by a couple of inches.

He ended up cussing me out by saying, “F*ck you Sam! Go watch some other match!” I was shocked by his outburst because I would never treat an elder in this manner. But after writing online for so long, I’m also used to the cussing, insults, and racist tirades I see against me and others online. It’s very similar to how some people get so angry at my household expenses and stringent rules for financial freedom.

My student ended up winning the match and apologizing, which I accepted. Sure, I wanted to yell back at him for being so disrespectful. But I trusted he would eventually come around to realizing that winning the right way is better than winning by cheating.

Losing the right way is also better than winning by cheating.

Nothing Beats The Satisfaction Of Succeeding On Your Own

Throughout my journey, I’ve encountered numerous adults born into wealthy households. While they possess ample free time courtesy of their riches, many lack fulfillment and meaning because they haven’t created their own wealth. Consequently, some create trust fund jobs to regain a sense of relevance.

Despite their desires for successful careers or the creation of personal fortunes, many find it challenging to surpass their parents’ financial success. This struggle often leads to a growing sense of emptiness. As parents, we must be careful not to give our children everything!

I spoke to a 34-year-old venture capitalist who lives in a $8 million house she bought four years ago. Amazing! She worked at a fintech company that IPOed then fell 90% over the next three years. She revealed she and her husband didn’t buy the house on their own. Her parents did.

Then she talked about feeling uneasy as a VC because she’s never built a company before or has had a successful exit. She constantly lives in self-doubt because so much of her wealth and opportunities were given to her. She even semi-joked whether her parents secretly donated to Stanford to get her in.

Embrace The Hard Mode Of FIRE And Stay Productive

Since leaving my day job in 2012, I can confidently assert that work holds significance. It’s one of the reasons why I’ve introduced and embraced fake retirement. Reach FIRE, but stay busy. Even for those with generational wealth, continuing to be productive in ways that also yield income is crucial for your mental health.

Though I am no longer financially independent, I welcome the challenge of reattaining financial independence by adhering to my first rule of FIRE. I’ve set a target date for June 15, 2029, at the age of 52. I aim to beat that deadline.

Retiring early with two kids in an expensive city presents greater challenges than doing so without children in a smaller town. But I welcome the challenge!

This time may be easier due to the presence of a larger Financial Samurai website, additional investments, and increased experience. Conversely, it may pose greater difficulty due to aging, heightened expenses, fading energy, another bear market, and the responsibilities of raising two children.

Regardless of the outcome, I am determined to appreciate the journey. I hope you do the same.

Reader Questions

Would you feel good about changing the rules of FIRE to win? If so, how do you overcome that uncomfortable feeling that you didn’t win the “right way”? Or maybe there is no right way, only your way on the path to financial independence.

Is changing the rules of FIRE similar to getting massive financial help from your parents in terms of a house, car, or college savings to get ahead? What about using your identity or connections to outperform others?

If You Want To Retire Early, Negotiate A Severance

If you plan to retire early and gain financial freedom, then you must read How To Engineer Your Layoff. The book teaches you how to negotiate a severance package. Given you wanted to quit anyway, there is no downside in trying to negotiate a severance.

I negotiated a six-figure severance that paid for five plus years of living expenses. It was my #1 catalyst to leaving his well-paying finance job behind. Think about a severance as giving you a financial runway during your transition or buying back time.

I incorporate all my wisdom and strategies on how to negotiate a severance package in his book. How To Engineer Your Layoff is now in its 6th edition as it’s continuously updated with new strategies and rules. Use the code “saveten” at checkout to save $10.

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site.

For more nuanced personal finance content, join 60,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009.

Discover more from Slow Travel News

Subscribe to get the latest posts sent to your email.