“I don’t want to have to work into my seventies,” says Rochelle White, who runs a marketing agency in Milton Keynes. The 38-year-old instead plans to retire at 56.

It’s an early target, but not that unusual. The popularity of the “Fire” movement — reaching financial independence and retiring early — has grown in recent years, as more workers dedicate their careers and investment portfolios to a single alluring goal: a 30 or even 40-year retirement.

“Since focusing on my pensions and retirement plan, I know what I need to do within [my] business to make my goals not only viable but a reality,” says White.

There are risks, of course. “Retiring early is an exciting but expensive business,” says Alice Guy, head of pensions and savings at investment platform Interactive Investor. “It needs careful planning to make your money last the distance.”

White’s first step was focusing on pension provision — the most attractive way of saving for retirement, particularly if you’re a higher-rate taxpayer now but likely to be paying 20 per cent in retirement.

In 2019, White didn’t know how much pension she had or where her old pensions were. So, she signed up to provider Penfold, found all her old pension information and consolidated them into one scheme. “That was a game-changer and it was easier to see what I had and where,” she says. Last year she started another private pension via Moneybox, and maintains an investment portfolio. “I know that I have money working for me, without me having to do much work — that is a great feeling.”

Most private pensions will not pay out until you reach 55; White will have to wait until she’s at least 57, since the minimum access age is set to rise in 2028. Being under 45, she’ll also have to wait longer to start drawing from her state pension. Currently set at 66, it is due to rise to 67 between 2026 and 2028; and to 68 between 2044 and 2046.

Anyone planning to retire at a younger age will need non-pension assets, such as Isas or buy-to-let property for income. Nevertheless, insurer SunLife surveyed 2,000 people in their fifties and found that 6 per cent had already retired. Of those still working, almost a third were planning to retire early, while the majority said they would do so, if money were no object.

Analysis by Interactive Investor found people are not only taking regular pension income much earlier than they were before the pandemic, but they are also taking their pension tax-free lump sum earlier too.

We asked FT readers to share their experiences. Michael Foster says he retired in his early thirties to Thailand, where he lives frugally, withdrawing 8 per cent a year from his investments in closed-end funds. “It’s been working for over a decade now. Initially, I retired on a scandalously low number, that financial advisers said would never work,” he says, admitting to “a figure well under £500,000”.

“Still, buying discounted funds with high-quality assets has worked out well so far, and while the future is always uncertain, I am so grateful for the ability to spend my thirties and, so far, half of my forties outside the rat race.”

A growing number of people in Foster’s generation and younger fear they may never be able to retire as they struggle with high housing costs, student loans and lower wages. In fact, more than a third of 35 to 54-year-olds admit that they don’t take an interest in their retirement savings, according to research from InvestEngine, an investment platform. The prospect of renting in later life is another hurdle: research from the Pensions Policy Institute cites the fall in home ownership among households aged 45-64 as one of the fastest growing risks to future retirement outcomes.

Even if they can afford to retire early, many decide not to. SunLife found the biggest reason for a delay is the concern that pension savings will run out.

To that end, financial advisers report one of their most common tasks is reassuring clients that they can afford to retire. Megan Rimmer, a chartered financial planner at Quilter Cheviot, says: “It’s a daunting process to go from having a regular income and saving money, to having no income and starting to spend the savings you have worked so hard to build during your lifetime.”

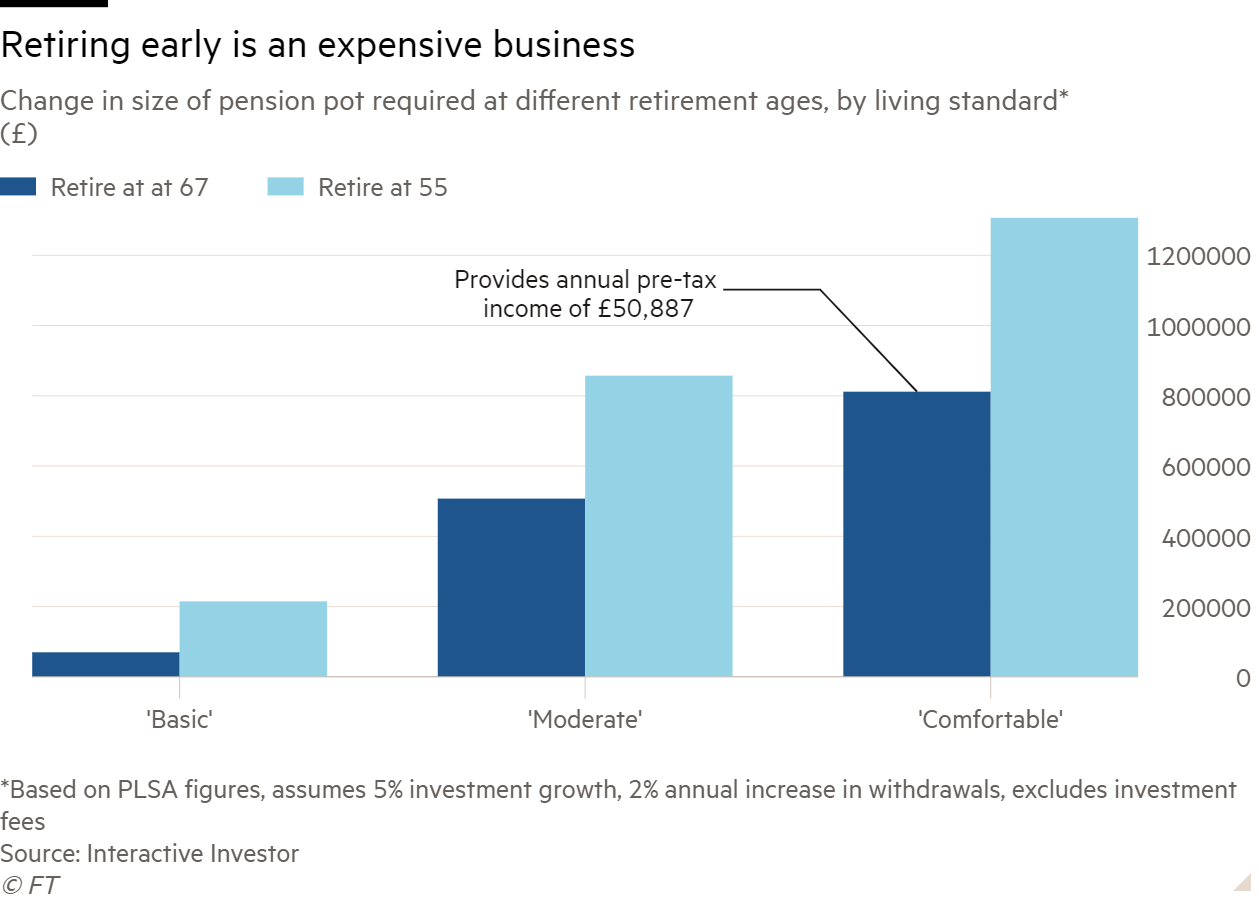

Research into what is known in the industry as the retirement living standards on behalf of the Pension and Lifetime Savings Association, sets out a “budget” for three retirement lifestyles.

The “minimum” level is £14,400 income a year for a single person and £22,400 for a couple; “moderate” is £31,300 for a single person and £43,100 for a couple; and the “comfortable” level is £43,100 for a single person and £59,000 for a couple.

But achieving these levels of income in your mid-50s is very different to achieving it at state pension age, when the full state pension of £11,502 a year kicks in — assuming you made the sufficient national insurance contributions. To live a comfortable retirement at 67, your pension pot needs to be a little over £810,000. Retire at 55 and you’d need £1.3mn, according to calculations by Interactive Investor, assuming 5 per cent investment growth on the fund, and 2 per cent annual increase in withdrawals.

Paying off the mortgage is often key to retiring early. Having some guaranteed income is also a major benefit.

FT reader Andy Triplett, from Wakefield, West Yorkshire, finished work on March 28, aged 57, to live a more active lifestyle. He had worked all his career in supply chains, most recently at ITM Power as a category manager.

“My mortgage was paid off last year. But my defined benefit (DB) pension from BAE Systems earlier in my career makes a big difference to my decision,” he says. “I also have an employer-provided Sipp that I transferred from Aviva to HL last year and a stocks and shares Isa too. I should have enough for 10 years. Then I’ll live off my DB pension and state pension. I’m lucky, I guess.”

“I’ve not scrimped and saved,” he adds. “But I did earn a good wage and put a bit extra into workplace pensions and my stocks and shares Isa — it had a snowball effect.”

For others, extreme frugality is a core part of achieving their aims: a “retire early at all costs” mentality.

By saving up to 70 per cent of annual income, followers of the Fire movement aim to achieve financial independence by living off the income from their accumulated funds. They aim to live in modest homes, sell unwanted possessions, even eschew car ownership. “The Fire movement tends to advocate fairly extreme saving strategies which won’t be realistic or desirable for lots of people,” says Tom Selby, director of public policy at investment platform AJ Bell.

Chris Palmer is 34 and is following the Fire movement strategy, with the goal of retiring early on between £750,000 and £1mn split between Isas and a Sipp. He lives in north Wales where he runs a web design company, plus a YouTube channel that dispenses investment tips. “I’m at around £250,000 now,” he says. “I have £130,000 in my Isa with Invest Engine, and £101,000 in my Sipp with Vanguard. I also use a Lifetime Isa with Hargreaves Lansdown, worth around £16,000.”

But he says the biggest challenge is balancing the impulse to spend now vs saving for the future. “Through my twenties I prioritised investing a lot, although I still travelled. And even now, I find it extremely hard not to fill my Isa. I’m buying a property soon and I had to take a year off from filling my Isa, which was surprisingly hard.

“The trouble is when you know £20,000 now could be worth £60,000 in retirement through investing, you don’t like to spend the money,” he says. “But I see more and more people who have died before reaching retirement, so you really need to make sure you are enjoying it now too.”

Another issue early retirees need to prepare for is uneven spending during retirement. The 4 per cent rule is widely known as being the amount you can withdraw “safely” from investments so they last 30-40 years. However, most people spend more at the beginning, when they are younger and active, and then less as they age and their world typically gets smaller. And then potentially they spend more again as their health declines in later years. Advisers call this the “retirement smile”.

Helen Morrissey, head of retirement analysis at Hargreaves Lansdown, warns: “If you want to do things like travel a lot in the early part of your retirement or maybe make a large purchase like buying a new car then these large early withdrawals could also take big chunks out of your pension that could mean you have to make tough budgeting decisions later on.”

Advisers recommend that cash flow planning is essential. This takes account of the complexities of money coming in and going out, plus the investment growth variables and different inflation scenarios. If you don’t have an adviser to help you do this, try a free financial planning tool such as Guiide.co.uk.

If you’re married, having the full picture of both yours and your partner’s finances can ensure you protect yourself as well as your loved ones. Advisers recommend forecasting each spouse’s financial situation if the other were to die. For example, your state pension ends when you die — and this can make up a key part of the household income. While Isa investments can be inherited by a spouse or civil partner, other pension incomes tend to be inherited at a reduced rate.

Unmarried couples need to take extra care, however, as you’re less likely to be able to inherit workplace pensions, especially those with defined benefits.

Inheritance tax could also be due on your partner’s estate — which wouldn’t be the case if you were married or in a civil partnership. Olivia Bowen, partner at financial planner Castlefield, says: “It’s not very romantic, but there are many tax advantages to getting hitched.”

Those who have taken the plunge and retired early say it’s important to have a “fall back” plan in case retirement doesn’t work out — either financially or emotionally. This may be downsizing your home or even returning to the workplace.

Tony Brent from Horsham, West Sussex, is 62, but retired in 2016 when he was 55 from his job as an IT consultant to play tennis four or five times a week. His wife Karen, also an IT consultant, retired at the same time to do volunteering. He says: “We pool all our money and stopped working, thinking we were OK financially even though we had two kids at university and one at school, but with a view we could go back to work if we needed to.”

After two years, Karen became bored of retirement, so went back to work as a technical author. And her husband says that could be an option for him too. “Even a year ago my old boss was asking if I could go back and do something. My skills are still marketable now,” he says.

This is important to Brent because although he made some good returns from his investments after Covid, he says, the uncertain geopolitical picture is making him nervous about his portfolio. “But having a house with no mortgage means our ultimate fall back is downsizing.”

While the thought of escaping the 9 to 5 may be attractive, unless you’re planning a very frugal retirement, for most, scaling down on work, rather than stopping completely, will be the more realistic option. This week, HSBC chief executive Noel Quinn announced he was retiring at 62, saying he needed “rest and relaxation”, and to achieve a better balance between his personal and business lives.

“It isn’t just about the money,” says Selby. “What do you plan to do with your time? Will you have enough going on to stimulate you?”

If your work has always been important to your sense of self, then it will probably be more important to you to replace it with something meaningful that supports your identity, albeit unpaid.

Mark Hurren is 46, based in Suffolk, and runs a specialist recruitment business Hurren and Hope, where he’s seen the need for a transition to retirement for the mental health benefits. “I’ve seen people who just stopped work and then got ill within a few years,” he says.

Hurren plans to retire at age 55, but plans to keep active: “Retirement for me is financial freedom, not sitting around on a deck chair reading the paper. It’s the ability to choose what I do,” he says. “I will only be retired from my first career — so it’s a chapter, rather than a full stop.”

Discover more from Slow Travel News

Subscribe to get the latest posts sent to your email.